Top 10 Education Loan for MBA in India 2026 | Interest Rates & Eligibility

March 24, 2026

Overview: An education loan for MBA in India helps you finance your top B-school dreams without upfront financial stress. With multiple banks and NBFCs offering flexible options, funding your MBA is now more accessible than ever.

Key Takeaways

- MBA education loans cover tuition, living, and academic expenses

- Interest rates typically range between 8% to 14%, depending on the lender and profile

- Collateral-free loans are available for all MBA institutes.

- Repayment tenure can go up to 10–15 years with a moratorium period

- Loan amounts can range from ₹20 lakhs to ₹1 crore+ based on the course and college

What You Will Learn in This Blog: Explore the best banks and NBFCs offering education loans for MBA in India, along with their interest rates, eligibility, and features.

Table of Contents

Why Take an Education Loan for MBA?

An MBA from a top-tier institute, IIMs, ISB, XLRI, FMS, SPJIMR, carries a fee structure that ranges from ₹10 lakh (FMS Delhi) to ₹35+ lakh (IIM Ahmedabad, ISB Hyderabad) for the two-year programme.

Add hostel, travel, books, and personal expenses, and the total cost of attendance can easily exceed ₹40–50 lakhs. For most middle-class families in India, self-financing is simply not practical.

That is where the best MBA education loan becomes a strategic tool rather than a last resort. Here is why financing through a structured education loan works in your favour:

- Near-100% cost coverage: Most banks fund tuition, hostel, travel, books, and even a laptop.

- Moratorium period: You pay nothing during your two-year MBA; repayment starts after graduation, plus a 6–12 month grace period.

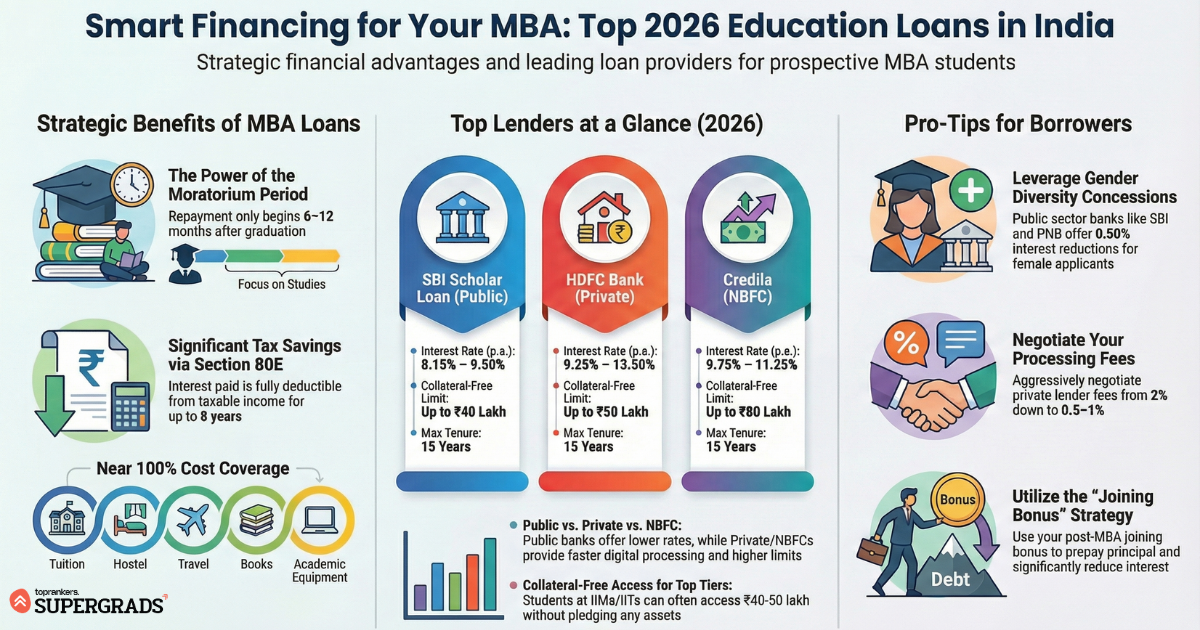

- Tax savings: Interest paid on your education loan is fully deductible under Section 80E for up to 8 years.

- Collateral-free options: Top IIM students can access up to ₹40 lakh without pledging any asset.

- No immediate liquid cash needed: Preserve your family's savings or investments.

- High ROI justification: Most IIM graduates repay their entire loan within 2–5 years, given typical placement salaries.

Top 10 MBA Education Loans at a Glance (2026)

The table below compares the current interest rates, maximum loan amounts, collateral requirements, and processing fees as of March 22, 2026. All rates are indicative and subject to change; always confirm with your lender before applying.

|

S.no |

Lender |

Type |

Max Loan Amount |

Interest Rate (p.a.) |

Collateral-Free Limit |

Processing Fee |

Repayment Tenure |

|

1 |

SBI Scholar Loan |

Public |

|

8.15% – 9.50% |

₹40 lakh (all mba institutes) |

Nil to ₹10,000 |

Up to 15 years |

|

2 |

Bank of Baroda Baroda Scholar |

Public |

₹60 lakh (List A/B); ₹30 lakh (IIM collateral-free) |

8.35% – 9.85% |

₹30 lakh (IIM-A/B/C, XLRI) |

Nil |

Up to 15 years |

|

3 |

Union Bank of India |

Public |

₹40 lakh (without collateral for premier institutes) |

8.40% – 10.05% |

₹40 lakh (premier) |

Nil |

Up to 15 years |

|

4 |

Punjab National Bank (PNB Saraswati) |

Public |

₹20 lakh (India); higher for abroad |

8.55% – 10.25% |

₹7.5 lakh |

Nil |

Up to 15 years |

|

5 |

Canara Bank IBA Model |

Public |

₹40 lakh (premier institutes) |

8.50% – 10.30% |

₹7.5 lakh (standard); ₹40 lakh (premier) |

Nil |

Up to 15 years |

|

6 |

HDFC Bank |

Private |

₹50 lakh (collateral-free); ₹1 cr (secured) |

9.25% – 13.50% |

₹50 lakh (premier institutes) |

1–2% |

Up to 15 years |

|

7 |

ICICI Bank |

Private |

₹1 crore+ |

9.50% – 10.50% |

₹50 lakh (select institutes) |

1–2% |

Up to 15 years |

|

8 |

Axis Bank |

Private |

₹40 lakh – ₹75 lakh |

10.00% – 12.75% |

₹40 lakh (premier) |

1–1.5% |

Up to 15 years |

|

9 |

Credila (formerly HDFC Credila) |

NBFC |

₹80 lakh (unsecured); No upper limit (secured) |

9.75% – 11.25% |

₹80 lakh |

1% + GST |

Up to 15 years |

|

10 |

Avanse Financial Services |

NBFC |

₹75 lakh (unsecured); higher with collateral |

10.50% – 13.00% |

₹75 lakh |

1–2% |

Up to 15 years |

⚠ Disclaimer: Interest rates, loan limits, and fees are indicative as of March 2026. Actual rates vary based on institute category, co-applicant profile, collateral offered, and the bank's internal risk assessment. Always verify current rates directly with the lender before applying.

Detailed Review: Top 10 Education Loans for MBA (2026)

#1 Best MBA Education Loan: State Bank of India (SBI) Scholar Loan Scheme

SBI remains the undisputed gold standard for the top 10 MBA education loans in India.

The Scholar Loan Scheme is tailor-made for premier management institutions and uses a four-tier institutional list (AA, A, B, C) to determine loan limits and rates.

For AA-list IIMs like IIM Ahmedabad, IIM Bangalore, IIM Calcutta, IIM Indore, etc., students can access up to ₹40 lakh without any collateral.

The interest rates for IIM-A students range from 8.05% to 8.15% p.a., making SBI the most cost-effective lender for top-ranked B-schools.

|

Parameters |

Details |

|

Max Loan (Collateral-Free) |

₹40 Lakh (IIMs) |

|

Max Loan (Secured) |

₹1.5 Crore |

|

Interest Rate |

8.15% – 9.50% |

|

Processing Fee |

Nil – ₹10,000 |

|

Repayment Tenure |

Up to 15 Years |

|

Moratorium |

Course Duration + 12 Months |

Best for: Students admitted to IIMs, IITs, XLRI, FMS, ISB, and other AA/A list institutes. Lowest interest rates among all lenders. Nil processing fee for most premier institutes. Pre-admission sanction available.

Also Read | How to Start MBA Preparation For CAT 2026 [Study Plan]

#2 Best MBA Education Loan: Bank of Baroda

Bank of Baroda's Baroda Scholar scheme is one of the most competitive MBA education loan products from a public sector bank.

For IIM-A, IIM-B, IIM-C, and XLRI students, the bank offers up to ₹30 lakh without any collateral, and up to ₹60 lakh for List A/B institutions when backed by security.

The scheme covers 100% of educational expenses, including tuition, hostel, travel, and study material, with zero margin money for select institutes.

|

Parameter |

Details |

|

Max Loan (No Collateral) |

₹30 Lakh (IIM-A/B/C) |

|

Max Loan (Secured) |

₹60 Lakh (List A) |

|

Interest Rate |

8.35% – 9.85% |

|

Processing Fee |

Nil |

|

Repayment Tenure |

Up to 15 Years |

|

Moratorium |

Course Duration + 12 Months |

Best for: Students in IIM-A, IIM-B, IIM-C, XLRI. Strong choice if SBI's institute category does not align. Nil processing fee is a key advantage over private lenders.

#3 Best MBA Education Loan: Union Bank of India

Union Bank of India is a strong contender for MBA students seeking a collateral-free education loan.

The bank offers up to ₹40 lakh without any collateral for students admitted to premier management institutes, with zero margin money, meaning the bank funds 100% of the cost.

Interest rates are highly competitive in the public sector bracket, and the bank has a dedicated relationship with several top IIMs and B-schools to streamline processing.

|

Parameters |

Details |

|

Max Loan (No Collateral) |

₹40 Lakh |

|

Interest Rate |

8.40% – 10.05% |

|

Margin Money |

Zero |

|

Processing Fee |

Nil |

|

Repayment Tenure |

Up to 15 Years |

|

Moratorium |

Course Duration + 12 Months |

Best for: Students seeking 100% funding with no out-of-pocket costs. Excellent for new IIM cohorts where on-campus bank branches facilitate faster sanction.

Also Read | Complete CAT Exam Syllabus

#4 Best MBA Education Loan: Punjab National Bank PNB Saraswati

PNB's Saraswati scheme is one of the oldest and most accessible MBA student loan options in India.

With a widespread branch network across Tier-2 and Tier-3 cities, PNB is particularly accessible for students from semi-urban backgrounds.

The interest rate concessions for female applicants (0.50%) make it attractive for women MBA candidates. The loan covers all study expenses, including hostel fees and travel.

|

Parameter |

Details |

|

Max Loan (India) |

₹20 Lakh |

|

Collateral-Free Up To |

₹7.5 Lakh |

|

Interest Rate |

8.55% – 10.25% |

|

Female Concession |

0.50% reduction |

|

Processing Fee |

Nil |

|

Repayment Tenure |

Up to 15 Years |

Best for: Female candidates (gender concession), students from smaller cities seeking easy branch access, or applicants whose institute does not fall in SBI's AA/A list.

#5 Best MBA Education Loan: Canara Bank

Canara Bank holds a special strategic position as the nodal bank for the PM-Vidyalaxmi scheme and the CSIS (Central Sector Interest Subsidy) scheme, both government-backed initiatives to make education loans more accessible to EWS and middle-income students.

As a regular lender, Canara Bank offers up to ₹40 lakh for premier management institutes, with competitive rates aligned to the IBA Model scheme.

|

Feature |

Details |

|

Max Loan (Premier) |

₹40 Lakh |

|

Interest Rate |

8.50% – 10.30% |

|

Govt Scheme Access |

CSIS + PM-Vidyalaxmi |

|

Processing Fee |

Nil |

|

Repayment Tenure |

Up to 15 Years |

|

Moratorium Period |

Course Duration + 12 Months |

Best for: Students from families with an annual income below ₹4.5 lakh (CSIS subsidy) or ₹8 lakh (PM-Vidyalaxmi 3% subvention). Also, a reliable choice for general applicants seeking a public sector lender with nationwide reach.

#6 Best MBA Education Loan: HDFC Bank Education Loan

HDFC Bank is the go-to private sector bank for MBA education loans when speed and convenience matter.

The bank offers quick approvals, a largely digital process, and collateral-free loans up to ₹50 lakh for select premier institutes.

The higher interest rate compared to public sector banks is offset by faster processing, fewer documentation hurdles, and the availability of pre-admission sanction, a major advantage when you need to confirm your seat quickly.

|

Features |

Details |

|

Max Loan (No Collateral) |

₹50 Lakh |

|

Max Loan (Secured) |

₹1 Crore |

|

Interest Rate |

9.25% – 13.50% |

|

Processing Fee |

1% – 2% of the loan amount |

|

Repayment Tenure |

Up to 15 Years |

|

Pre-Admission Sanction |

Yes |

Best for: Students who need fast approval and a digital-first process. Suitable if your institute is not in SBI's premier list but is recognised by HDFC Bank. Negotiate the processing fee down aggressively.

Also Read | Let's Find Out Which IIM is best for MBA

#7 Best MBA Education Loan: ICICI Bank Education Loan

ICICI Bank stands out as the preferred lender when the required loan amount exceeds ₹50 lakh, particularly relevant for MBA programmes abroad (Wharton, LBS, INSEAD, etc.) or for expensive domestic executive MBA programmes.

The bank offers loans of ₹1 crore and above, collateral-free up to ₹50 lakh for selected premier institutes.

Its robust digital platform and instant, pre-approved loans for existing account holders make it a convenient option.

|

Features |

Details |

|

Max Loan Amount |

₹1 Crore+ |

|

Collateral-Free Up To |

₹50 Lakh |

|

Interest Rate |

9.50% – 10.50% |

|

Processing Fee |

1% – 2% of the loan amount |

|

Repayment Tenure |

Up to 15 Years |

|

Pre-Admission Sanction |

Yes |

Best for: Students targeting MBA programmes abroad or high-cost executive MBAs in India requiring over ₹50 lakh. Also excellent for ICICI Bank existing customers who may receive pre-approved offers.

#8 Best MBA Education Loan: Axis Bank Education Loan

Axis Bank offers a customisable education loan product that allows students to tailor repayment terms to their expected post-MBA income trajectory.

With loans up to ₹75 lakh and a streamlined online application, Axis Bank is a strong choice for students from institutes that may not be in the top tier but still warrant significant funding.

The bank does not charge prepayment penalties, making it flexible for students who receive large joining bonuses.

|

Feature |

Details |

|

Max Loan Amount |

₹40–75 Lakh |

|

Interest Rate |

10.00% – 12.75% |

|

Prepayment Penalty |

None |

|

Processing Fee |

1% – 1.5% |

|

Repayment Tenure |

Up to 15 Years |

|

Margin Money |

Zero Required |

Best for: Students who anticipate large joining bonuses and want zero prepayment penalty. Suitable when flexibility in EMI restructuring is a priority.

#9 Best MBA Education Loan: Credila Financial Services

Credila (formerly HDFC Credila) is India's first and largest dedicated education loan NBFC.

Having funded over 2.26 lakh students across 5,200+ institutions in 64 countries, Credila combines deep expertise in education lending with flexible, fully customised loan products.

For MBA aspirants, Credila is particularly useful when targeting a global MBA or when public-sector banks have stricter institute eligibility criteria. Unsecured loans go up to ₹80 lakh, and the pre-admission evaluation feature is a major advantage.

|

Feature |

Details |

|

Max (Unsecured) |

₹80 Lakh |

|

Max (Secured) |

No Upper Limit |

|

Interest Rate (Secured) |

9.75% onwards |

|

Interest Rate (Unsecured) |

11.25% onwards |

|

Processing Fee |

1% + GST |

|

Tax Benefit |

Section 80E |

Best for: Global MBA aspirants (US, UK, Canada, Europe). Students requiring pre-admission loan letters for visa processing (I-20 for the USA). No prepayment charges. Rates are floating, and negotiate the spread carefully.

#10 Best MBA Education Loan: Avanse Financial Services

Avanse Financial Services has carved out a niche as the most flexible and accessible NBFC for education loans, particularly for students who are rejected elsewhere due to borderline credit profiles or non-standard institutes.

The acceptance rate at Avanse is notably higher than that of competitors, and it is known to approve loans for students even without an offer letter in some cases, making it a practical safety net for students whose CIBIL or co-applicant profile may not meet stringent public-sector criteria.

|

Features |

Details |

|

Max (Unsecured) |

₹75 Lakh |

|

Interest Rate |

10.50% – 13.00% |

|

Acceptance Rate |

High (flexible) |

|

Processing Fee |

1% – 2% |

|

Repayment Tenure |

Up to 15 Years |

|

Institutions Covered |

3,000+ (50+ countries) |

Best for: Students who have been rejected by banks due to credit score or income issues. Borrowers with non-standard co-applicant profiles. Rates are risk-based; two students at the same college may get different rates.

Who Is Eligible for an MBA Education Loan?

Eligibility for the best education loan for MBA in India is broadly standardised across lenders, but key criteria can vary. Here is what most banks require:

- Indian Citizenship: The applicant must be an Indian national.

- Age: Usually 16 to 35 years at the time of application. Some NBFCs go up to 45.

- Academic Record A minimum of 50%–60% marks in prior qualifications (graduation). Higher marks help secure better interest rates.

- Admission Proof: A confirmed admission offer letter from a recognised MBA or PGDBM programme.

- Co-Applicant: A parent, guardian, or spouse must act as a co-borrower with a healthy CIBIL score (ideally 700+) and steady income.

- Co-Applicant Income: Most banks prefer a co-applicant with a net monthly income of ₹25,000–₹50,000, depending on the loan size.

Read More| Detailed strategy of CAT Exam Preparation

Documents Required for MBA Education Loan

Keep these documents ready before you approach any lender to avoid delays in processing your MBA loan application:

- Admission Offer Letter: Official letter from your B-school specifying your name, course, and programme duration.

- Academic Records, Marksheets from Class 10, Class 12, and graduation. CAT/GMAT/GRE scorecard.

- KYC Documents: Aadhaar card, PAN card, and passport (both applicant and co-applicant).

- Passport-size Photographs: Recent photos of both applicant and co-applicant.

- Income Proof (Co-Applicant): Last 6 months' salary slips/bank statements; last 2 years' ITR.

- Address Proof: Utility bill, Aadhaar, or any government-issued address document.

- Fee Structure Document: Official fee schedule from the institute (tuition + hostel + other expenses).

- Collateral Documents (if applicable): Property papers, fixed deposit receipts, or insurance policy documents.

Repayment, Moratorium Period & Tax Benefits

How Repayment Works?

One of the most student-friendly aspects of the MBA education loan structure in India is the built-in moratorium period.

During your 2-year MBA programme plus 6–12 months after graduation, you are not required to make principal repayments.

However, interest does accumulate during this period; you can pay it off to reduce the overall burden, or let it be added to the principal.

Once the moratorium ends, repayment begins via EMIs. Typical EMIs for a ₹20–25 lakh loan over 10 years range from ₹20,000–₹30,000 per month, a manageable amount given IIM placement salaries that often start at ₹20–35 lakh per annum.

Many graduates use their joining bonus to prepay a large chunk of the principal, significantly reducing their effective interest burden.

Tax Benefits Under Section 80E

This is one of the most underutilised advantages of an MBA education loan. The entire interest component of your EMI is deductible under Section 80E of the Income Tax Act with no upper cap on the deduction amount.

This benefit is available for up to 8 consecutive years from the start of repayment. For someone repaying a ₹25 lakh loan at 9% interest, the annual tax savings can amount to ₹50,000–₹1 lakh depending on the tax bracket.

📊 Repayment Reality Check

According to industry data, most IIM graduates repay their education loan in 2–5 years, well within the 15-year tenure offered by banks.

Students in top-50 MBA colleges take 5–8 years on average. The joining bonus from placements often covers 30–50% of the outstanding principal on Day 1 of employment.

Pro Tips to Get the Best Education Loan Deal

1. Choose Floating Rate Loans

Floating rates are linked to the bank's base rate. When the RBI cuts rates, your interest cost drops, a significant benefit over a 10–15-year tenure.

2. Leverage Work Experience

If you have 2+ years of professional experience before your MBA, many lenders, especially NBFCs, will offer a 0.25%–0.50% reduction in your interest rate.

3 Gender Diversity Concession

Most public sector banks, SBI, PNB, BOB, offer a 0.50% interest concession for female candidates. Always ask for it explicitly during the application.

4 Negotiate Processing Fees

Public sector banks often waive processing fees entirely. For private banks and NBFCs, you can often negotiate from 2% down to 0.5–1% by applying through a loan aggregator or channel partner.

5 Aim for Zero Margin Money

Some banks ask you to fund 5–10% of the total cost yourself (margin money). Banks like SBI, Union Bank, and Credila offer zero margin for premier institutes, ensuring 100% coverage.

6 Use Joining Bonus Strategically

Most MBA graduates receive a joining bonus of ₹2–10 lakh. Prepaying principal with this bonus can save years of interest payments. Choose lenders with zero prepayment penalty.

Government Schemes & Subsidies (2026)

1. PM-Vidyalaxmi Scheme

The PM-Vidyalaxmi scheme provides collateral-free and guarantor-free education loans for meritorious students admitted to QHEIs (Quality Higher Education Institutions).

For students with an annual family income of up to ₹8 lakh, a 3% interest subvention on loans up to ₹10 lakh is available.

The subsidy amount is credited directly to the beneficiary's loan account via the PM Vidyalaxmi Digital Rupee App. Canara Bank is the nodal bank for this scheme.

2. Central Sector Interest Subsidy (CSIS) Scheme

Operational since 2009, the CSIS scheme offers a full interest subsidy during the moratorium period to students from economically weaker sections with an annual family income of up to ₹4.5 lakh.

The subsidy covers only professional and technical courses from NAAC-accredited or NBA-approved institutions, making it directly applicable to MBA programmes at recognised B-schools.

🏛️ How to Apply?

Both PM-Vidyalaxmi and CSIS applications are processed digitally at pmvidyalaxmi.co.in. The process is entirely online; no physical visits to government offices are required.

Apply simultaneously with your bank loan to avoid delays.

Beyond Loans: Scholarships & Alternative Funding

While the top 10 education loans for MBA options above cover most of your financing needs, smart students layer multiple funding sources to minimise debt. Here are the most effective alternatives:

1. Merit & Need-Based Scholarships

Most top IIMs, ISB, XLRI, and SPJIMR offer scholarships based on academic performance, family income, gender, and state of domicile. High achievers have covered 100% of their tuition through these awards.

2. Corporate & Foundation Scholarships

Companies like Tata Trusts, Aditya Birla Group, Infosys Foundation, and several PSUs offer MBA scholarships ranging from ₹1 lakh to ₹ 5 lakh per year.

3. Summer Internship Stipends:

Stipends at top IIM placements can reach ₹1–1.5 lakh per month. A 2-month internship alone can generate ₹2–3 lakh to prepay your loan principal.

4. Case Competition Prize Money

Winning corporate case competitions (Tata Crucible, HUL LIME, BCG Potter) can fetch ₹1–2 lakh per event. Serious participants compete in 5–8 competitions per year.

5. Part-Time Freelance Work

MBA programmes do not prohibit students from freelancing in their area of expertise. Consulting or writing projects can supplement income during the programme.

It's Always "IIM-Possible"

The cost of an MBA should never be the reason you don't pursue one. With the top 10 MBA education loans detailed in this guide, from SBI's unbeatable rates for IIM students to Credila's global coverage for international programmes, there is a financing solution tailored to every profile and ambition.

Combine a well-negotiated loan with internship earnings, scholarships, and Section 80E tax savings, and your MBA investment becomes not just manageable, but genuinely smart. Start early, compare carefully, and fund your future with confidence.

Frequently Asked Questions

Which is the best education loan for MBA in India in 2026?

What is the interest rate for an MBA education loan in 2026?

Do I need to start repaying during my MBA?

Which bank is best for an MBA education loan for IIMs?

How long does it take to repay an MBA education loan?

Lalita Vishwakarma

Content Writer

SHARE